Navient Earnings Preview: Key Metrics and Future Outlook

As Navient, a prominent player in the financial services sector, gears up to announce its latest earnings results, investors, analysts, and borrowers alike are keen to understand the company's current performance and future trajectory. Headquartered in Wilmington, Delaware, Navient has undergone significant transformations since its inception in 2014 as a spin-off from SLM Corporation (Sallie Mae). With a legacy rooted in facilitating access to higher education financing, the company now navigates a complex landscape characterized by evolving regulatory pressures, strategic shifts, and ongoing legal challenges. This preview delves into what to anticipate from Navient's upcoming earnings report, examining key financial metrics, recent operational shifts, and the broader outlook for the company.

Understanding Navient: A Brief History and Evolving Business Model

Navient’s history is deeply intertwined with student loan financing, boasting roots that stretch back over five decades. Initially formed to manage Sallie Mae's consumer banking and loan servicing operations, Navient quickly established itself as a major force in student loan servicing, asset management, and business processing solutions tailored for the education, healthcare, and government sectors. The company has, at various points, serviced portfolios encompassing trillions in student loans for millions of borrowers, leveraging technology to enhance repayment management and operational efficiency.

A defining characteristic of Navient's strategy has been its significant involvement in the private student loan market, notably through acquisitions like Earnest, which bolster its direct lending capabilities. However, recent years have seen Navient actively pivot towards diversifying its revenue streams, a strategic move largely influenced by declining federal servicing contracts and heightened regulatory scrutiny. This diversification effort aims to reduce reliance on student loan servicing and explore growth opportunities in other business processing avenues. For a deeper dive into the company's journey and pivotal shifts, consider reading

Navient Unpacked: From Sallie Mae to Federal Loan Ban.

Recent Performance and Analyst Expectations

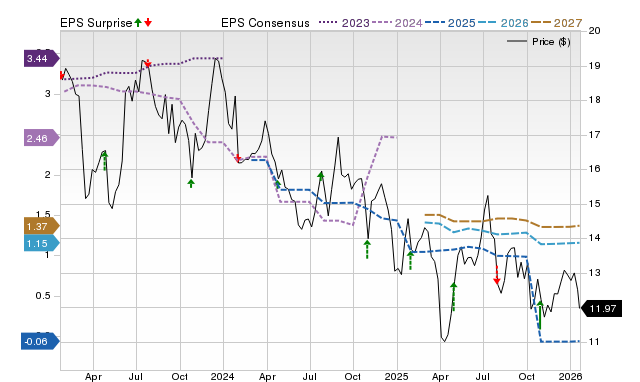

Examining Navient's recent financial performance provides crucial context for the upcoming earnings report. In its last quarter, Navient surpassed analysts’ revenue expectations by 3.8%, reporting revenues of $169 million. However, this figure represented a substantial 62.6% year-on-year decline, indicating a slower period for the company. Furthermore, the quarter was marked by a significant miss of analysts' earnings per share (EPS) estimates, signaling challenges in profitability despite the revenue beat.

Looking ahead to the current quarter, analysts project Navient's revenue to decline by 4.4% year-on-year, reaching approximately $155.8 million. While still a decline, this forecast suggests an improvement compared to the steeper 43.4% decrease recorded in the same quarter last year. Adjusted earnings are expected to come in at $0.31 per share. Interestingly, analysts covering Navient have largely reconfirmed their estimates over the past 30 days, suggesting a consensus that the business will maintain its current trajectory. Investors should note that Navient has missed Wall Street’s revenue estimates in five of the last eight quarters, underscoring a pattern of unpredictability in its top-line performance.

Navigating the Legal and Regulatory Landscape

Navient’s operational landscape has been significantly shaped by a series of legal challenges and regulatory actions. The company has faced numerous allegations of servicing failures, including claims of steering borrowers into costlier repayment options and mismanaging forbearance applications. These controversies culminated in a landmark settlement with the Consumer Financial Protection Bureau (CFPB) in September 2024. This agreement imposed a permanent ban on Navient from servicing federal student loans and mandated a $120 million redress to affected borrowers.

Beyond the federal actions, Navient has also been the subject of multiple state-led lawsuits and investigations. These cases have often highlighted alleged patterns of deceptive practices in both loan origination and collections, leading to multistate settlements totaling hundreds of millions of dollars. While Navient has consistently contested many of these claims, asserting that empirical repayment data supports its practices, the financial and reputational impact of these legal battles cannot be overstated. The ongoing implications of these settlements for borrowers are significant; if you believe you might be owed a payout, exploring resources like

Navient Student Loan Settlements: Are You Owed a Payout? could be beneficial. The permanent exit from federal student loan servicing marks a pivotal moment, forcing Navient to accelerate its strategic shift towards private lending and diversified business processing.

Peer Comparison and Market Sentiment

To gain a broader perspective on Navient's position, it's helpful to compare its performance with that of its peers within the consumer finance segment. Some competitors have already reported their Q4 results, offering potential insights into market trends. For instance, Sallie Mae, a direct competitor and Navient's former parent company, delivered a robust 16.4% year-on-year revenue growth, outperforming analysts’ expectations by 1%. Similarly, Ally Financial reported revenues up 3.7%, topping estimates by 0.9%. Following these results, Sallie Mae's stock traded up 6.2%, while Ally Financial saw a 1% decline.

Overall, investors in the consumer finance sector have maintained a relatively stable outlook leading into recent earnings reports, with share prices remaining flat over the past month. In contrast, Navient’s stock has experienced a 4.2% decline during the same period. The company heads into its earnings announcement with an average analyst price target of $13.06, which currently stands above its share price of approximately $12.10. This discrepancy could suggest that analysts see some potential upside, or it might reflect a delayed reaction to recent challenges and strategic adjustments. Investors will be closely watching for any management commentary that might bridge this gap.

Key Metrics to Watch and Future Outlook

When Navient releases its earnings, several key metrics will warrant close attention:

*

Revenue and EPS: Beyond the headline numbers, investors should scrutinize the drivers behind these figures. Is the revenue decline stabilizing as projected? Are the missed EPS estimates a one-off or indicative of deeper profitability issues?

*

Segment Performance: Given Navient’s strategic pivot, detailed reporting on its diversified revenue streams, particularly from private lending (like Earnest) and business processing for healthcare and government sectors, will be crucial. Is the company successfully growing these segments to offset the loss of federal servicing?

*

Asset Quality and Loan Portfolio Health: Any updates on the performance of its private loan portfolios, including delinquency rates, charge-offs, and payment behaviors, will provide insight into the underlying health of its assets in a challenging economic environment.

*

Forward Guidance: Management’s outlook for the coming quarters—particularly regarding revenue growth targets for non-student loan segments, cost management initiatives, and capital allocation strategies—will be critical for assessing Navient's future profitability and strategic direction.

Navient's future outlook hinges significantly on its ability to effectively execute its diversification strategy while managing the lingering effects of its past legal entanglements. The permanent ban from federal student loan servicing fundamentally reshapes its operational model, pushing it more firmly into the private sector and business processing. Success will depend on its capacity to leverage existing technological infrastructure, maintain operational efficiency, and build trust within its new target markets.

In conclusion, Navient stands at a pivotal juncture. Its upcoming earnings report will offer a clearer picture of how effectively it is navigating the choppy waters of regulatory pressures and strategic realignment. While challenges persist, particularly concerning its historical legal issues and the ongoing revenue transition, the company’s strategic pivot towards diversified services could unlock new growth avenues. Investors will be seeking tangible evidence that this transformation is yielding positive results and setting the stage for sustainable long-term value.